The adjusted trial balance for Bold City Consulting is presented in Figure 1. The adjustments need to be made in the trial balance for the above details. The adjusting entries for the first 11 months of the year 2015 have already been made.

- After posting the above entries, the values of some of the items in the unadjusted trial balance will change.

- The preparation of the adjusted trial balance is the sixth step of the accounting cycle.

- Once all ledger accounts and their balances are recorded, thedebit and credit columns on the adjusted trial balance are totaledto see if the figures in each column match.

- Using accounting software like QuickBooks Online can do all these tasks for you behind the scenes.

- Financial statements drawn on the basis of this version of trial balance generally comply with major accounting frameworks, like GAAP and IFRS.

- After incorporating the adjustments above, the adjusted trial balance would look like this.

Latest blog posts

To simplify the procedure, we shall use the second method in our example. As with all financial reports, trial balances are always prepared with a heading. Typically, the heading consists of three lines containing the company name, name of the trial balance, and date of the reporting period.

How to Prepare an Accurate Adjusted Trial Balance

Prepaid expenses are payments made in advance for goods or services to be received in the future. Initially recorded as assets, these payments require adjustments to reflect the portion that has been consumed or expired during the accounting period. To adjust for prepaid expenses, an entry is made to debit the appropriate expense account and credit the prepaid asset account. This process ensures that expenses are recognized in the period they are incurred, aligning with the matching principle of accounting.

Financial Accounting

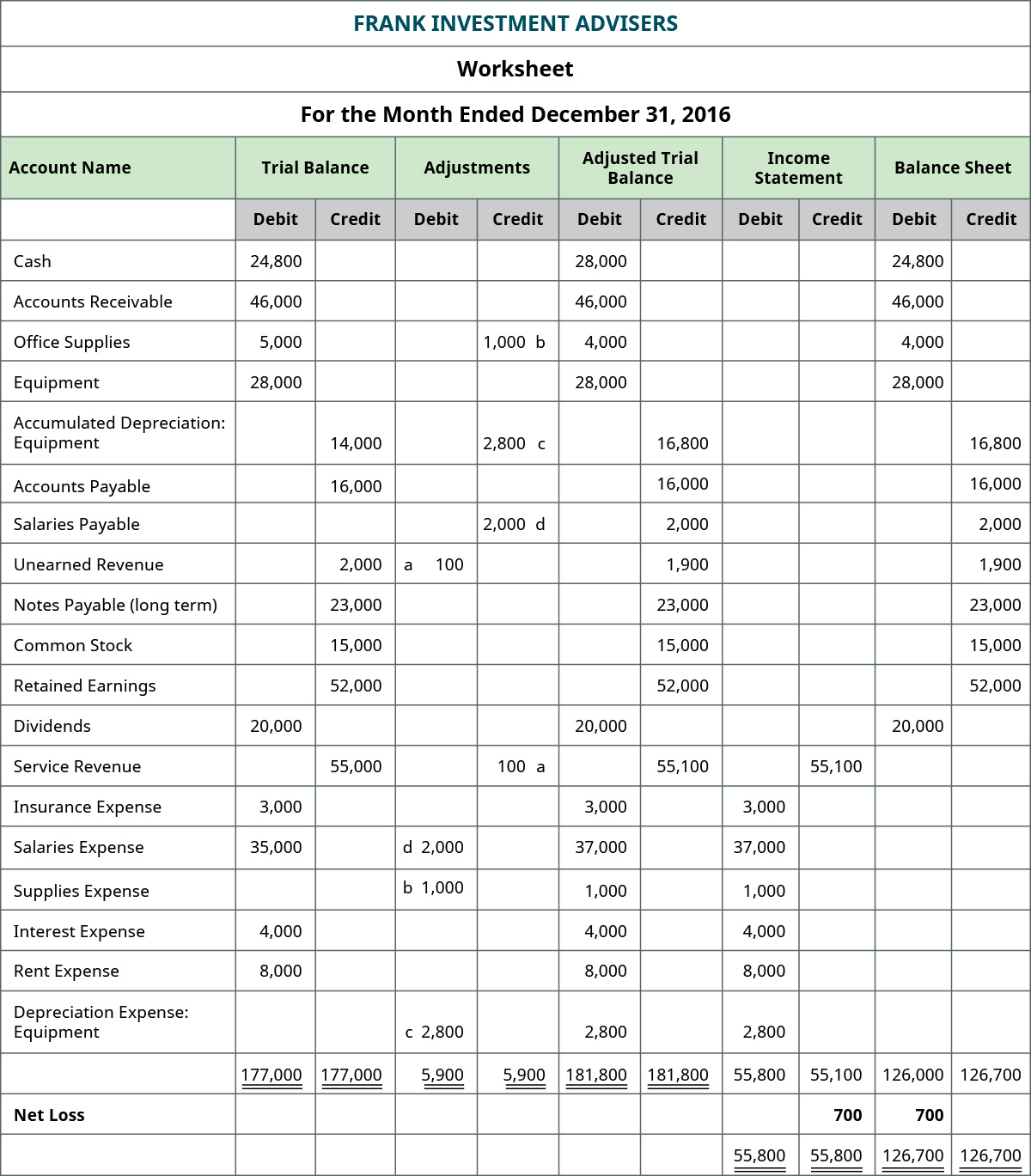

The adjusted trial balance is a key tool in the accounting process, ensuring that all financial transactions are recorded and adjusted before preparing financial statements. It acts as a checkpoint, allowing accountants to verify that total debits equal total credits after adjustments. This balance reflects the true financial position of a business at a specific point in time. Adjusted trial balances are prepared at the end of the accounting cycle and are used to help prepare the financial statements for the period.

Creating an adjusted trial balance is a critical step in ensuring that a company’s financial statements are accurate and reliable. By adjusting the trial balance for accrued revenues, expenses, and other necessary items, you can ensure that your financial records reflect the true state of the business. This process helps in preparing accurate financial statements and detecting any discrepancies in the accounting records. Depreciation is the systematic allocation of the cost of a tangible fixed asset over its useful life. This adjustment is necessary to account for the wear and tear, obsolescence, or reduction in value of an asset over time. To record depreciation, an adjusting entry is made to debit a depreciation expense account and credit an accumulated depreciation account, which is a contra-asset account.

How to Prepare an Adjusted Trial Balance

The adjusted balances are summed to become the adjusted trial balance. Once all of the adjusting entries have been posted to thegeneral ledger, we are ready to start working on preparing theadjusted trial balance. Preparing an adjusted trial balance is thesixth step in the accounting cycle. An adjusted trialbalance is a list of all accounts in the general ledger,including adjusting entries, which have nonzero balances.

To account for accrued revenues, an adjusting entry is made to recognize the income in the period it was earned, rather than when cash is received. This involves debiting an asset account, such as Accounts Receivable, and crediting a revenue account. By doing so, the financial statements reflect the true revenue generated during the period, providing a more accurate picture of the company’s performance. This adjustment is crucial for businesses that operate on credit terms, as it ensures that all earned income is captured in the financial records, aligning with the accrual accounting principles.

Once all necessary adjustments are made, a new second trial balance is prepared to ensure that it is still balanced. An adjusted trial balance is a trial balance which is prepared after the preparation of adjusting entries. Adjusted trial balance contains balances of revenues and expenses along with those of assets, liabilities and equities. Adjusted trial balance can be used directly in the preparation of the statement of changes in stockholders’ equity, income statement and the balance sheet. However it does not provide enough information for the preparation of the statement of cash flows. Adjustments in trial balances ensure that financial statements accurately reflect a company’s financial position.

As you have learned, the adjusted trial balance is an importantstep in the accounting process. But outside of the accountingdepartment, why is the adjusted trial balance important to the restof the organization? An employee or customer may victims of texas winter storms get deadline extensions and other tax relief not immediatelysee the impact of the adjusted trial balance on his or herinvolvement with the company. The next type of adjustment is the accrual, which ensures inclusion of the future payments that the business entity is entitled to make.

The balance of Accounts Receivable is increased to $3,700, i.e. $3,400 unadjusted balance plus $300 adjustment. Service Revenue will now be $9,850 from the unadjusted balance of $9,550. Here, the adjustment will be $ 50,000.00 as the rent deposit is $ 20,000, the rent payment will be $ 30,000. Here, the adjustment will be $ 80,000.00 as the total salary payable is $ 80,000. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

The list and the balances of the company’s accounts are presented after the adjusting journal entries are made at the year-end. In our detailed accounting cycle, we just finished step 5 preparing adjusting journal entries. We will use the same method of posting (ledger card or T-accounts) we used for step 3 as we are just updating the balances. Remember, you do not change your journal entries for posting — if you debit in an entry you debit when you post.